Consistent Range Chop is Ideal Weather For Time Spreads

SPX/QQQ term spread trades utilizing event premium

This market has gone nowhere for weeks in a very tight range:

And lately SPX our calendar spread trades have been quick hitters with superb results:

Even better results in QQQ by utilizing giga tech earnings vol:

So, back to the well, this time utilizing NFP vol and CPI vol to acquire longer dated vol on the cheap. The first set will be selling NFP vol to own CPI vol and the second set will be utilizing CPI vol to own cheap holiday week vol.

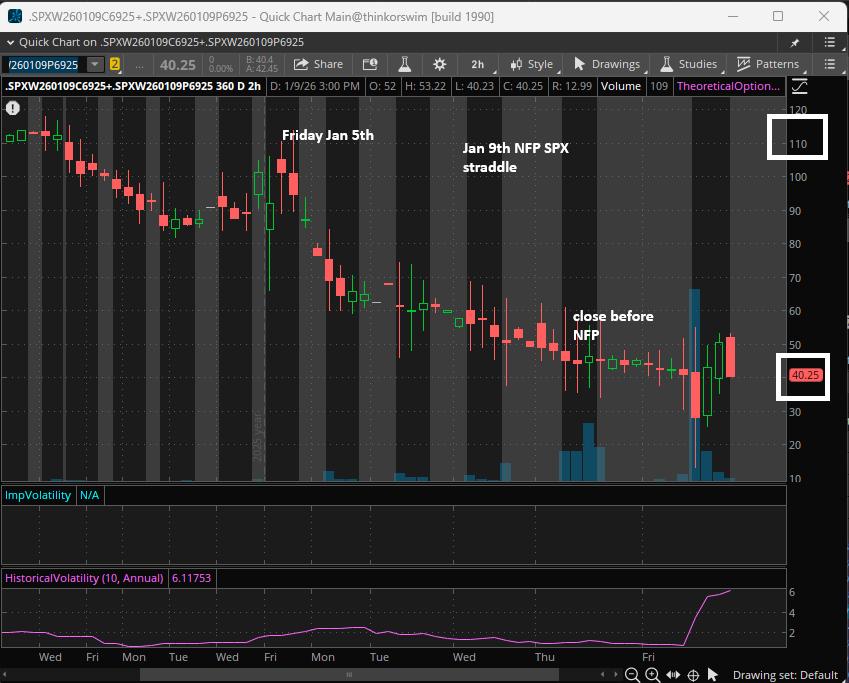

Looking at NFP vol, as I’ve trumpeted ad nauseum here, the short vol mafia and non-discretionary/formulaic/ETF vol sellers like to suck the event vol out of the market before the event, which then frees up the market to move on event day without the restriction of excess residual premium, that on event day would be sold to hold price in check.

Here is a chart of the 6925 Jan 9th payrolls straddle as it was whittled down from $110 the Friday before to $43 the night before the report:

What resulted that day was a move of +60 SPX, so the straddle was profitable most of the day, multiple opportunities to sell it for 55pts, if you didn’t leave it lying around vulnerable to the .1DTE last half hour crowd and their games.

And here is the same strike straddle for this Friday:

Keep reading with a 7-day free trial

Subscribe to Smashing Volatility to keep reading this post and get 7 days of free access to the full post archives.