Time To Do Some Hedging Trades?

They are quite cheap historically as implied vol seasonality gets trashed

“This has been a market where you’ve been paid to be irresponsibly bullish, period.” Tony Pasquariello of the vampire squid GS.

With euphoria gripping prices across the markets in the everything rally/perma bubble, it certainly feels like (plenty of evidence incoming) we just witnessed a long capitulation moment last week. Coincidentally, or not, implied vol hasn’t been this low at this time of year since 2017 (before volmageddon of course). The cacophony of ‘don’t fight the Fed’ is one awfully loud mob; a CNBC don’t fight the Fed drinking game would put you under the table by 11am. So, I’m supposing it’s time:

(The famous IBKR dinner hedger lady)

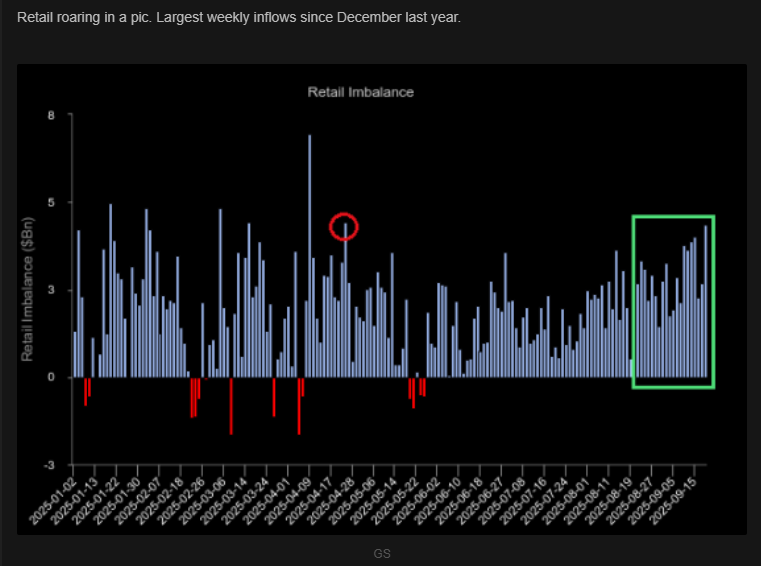

Let’s start with the retail army; to say they are the largest force in markets lately is not hyperbole, it’s defensible. This cohort has poured money into the market for 20 straight months and 19 of the last 22 weeks. And last week, they simply shoveled in more money than at any time since last December:

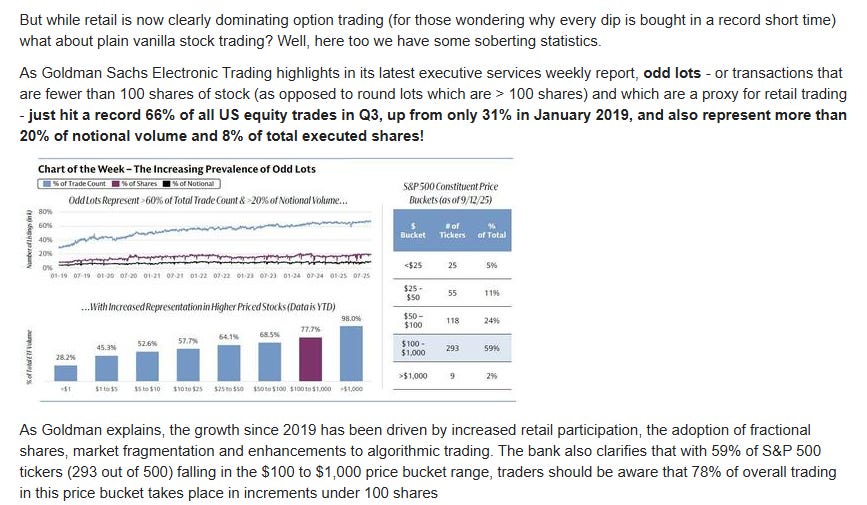

And specifically to my point that they are now the not so invisible hand that drives markets higher, this next graphic should greatly augment the case. Retail now makes up 2/3rds of transaction volume which is more than double what it was 5 years ago:

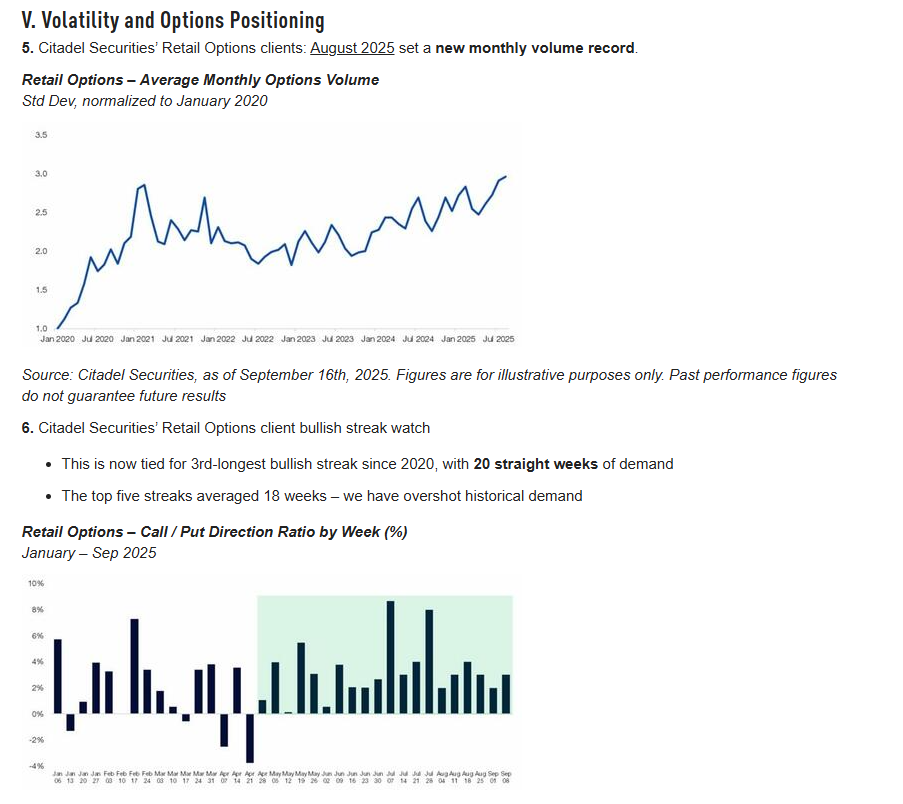

And option volumes, well that chart alone has its own convexity, the growth in 0DTE is stunning, now making up over 60% of daily options volume. And, guess who’s the fueling factor in that arena, you guessed it:

Longest streak of option buying since grandma Yellen’s twisteroo/treasury QRA easing in October 2023, and of course on record retail options volume. And there has been so much winning on this front, buying calls and yes, selling puts.

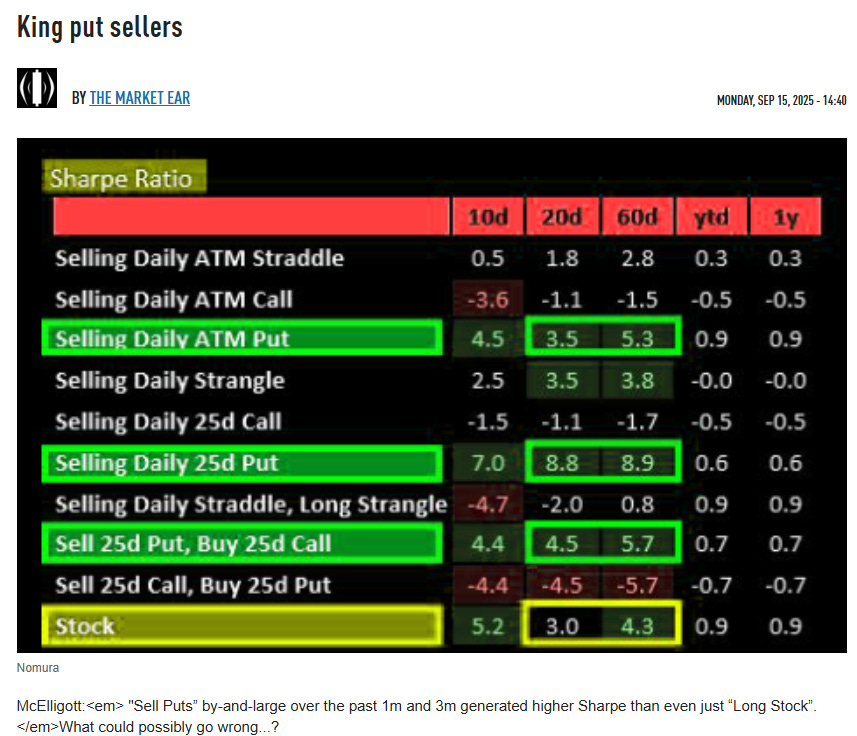

Retail has become a major vol smashing swarm, printing their own homemade QE every day, with sharpe ratios that are far greater than trading stocks:

Selling 25 delta puts is making Madoff’s sharpe ratio look like rookie-ville. I call this the $100 in the mailbox effect. If you went to the mailbox for three days in a row and there was a $100 bill in it, you would be insane not to go to the mailbox tomorrow.

So, this behavior has a lot of momentum, it is reflexive in that it supports the market on down days, and don’t expect it to peter out just because they might have a bad day, which hasn’t happened since the first day of September. Yet, this crowd will be taught a very valuable lesson in shorting naked vol at some point. Naked puts can put your account out of business on that one day - it’s not like we haven’t seen mini volmageddons over the last couple years.

From the call side, as I explained in a post a couple months ago, retail traders are becoming far more sophisticated, using their own algorithms to trade calls at specific times of the day:

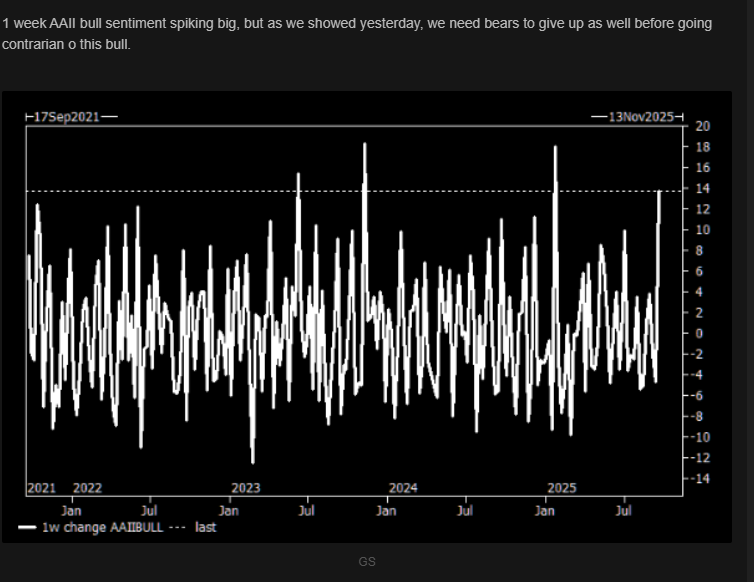

From a sentiment perspective, individual investors just saw one of the largest spikes in bullishness in quite some time:

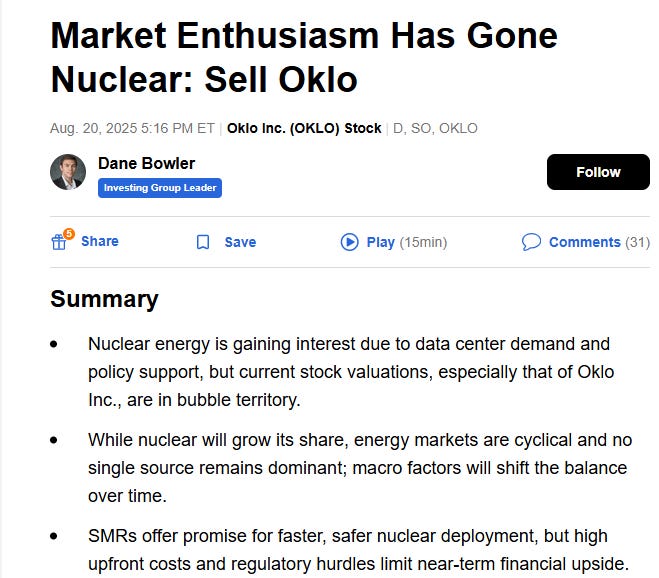

The stonks retail loves the most have gone parabolic. Nuclear stocks, eons away from actually earning actual profits for investors….whoa, let me step back. Ahem, years away from generating any actual revenues, 2028 to start, 2030 for SMRs to be potentially deployed in size, this price action screamed of a news fueled combination of opex/calls open interest, leveraged ETFs, (yes, OKLL 2x ETF) and retail excitement:

They have zero revenues, burn a lot of cash and will need a lot more, so it begs for a capital raise right here. I mean, 70% lower a whole month ago, folks were calling it a bubble stonk then:

https://seekingalpha.com/article/4815407-market-enthusiasm-has-gone-nuclear-sell-oklo

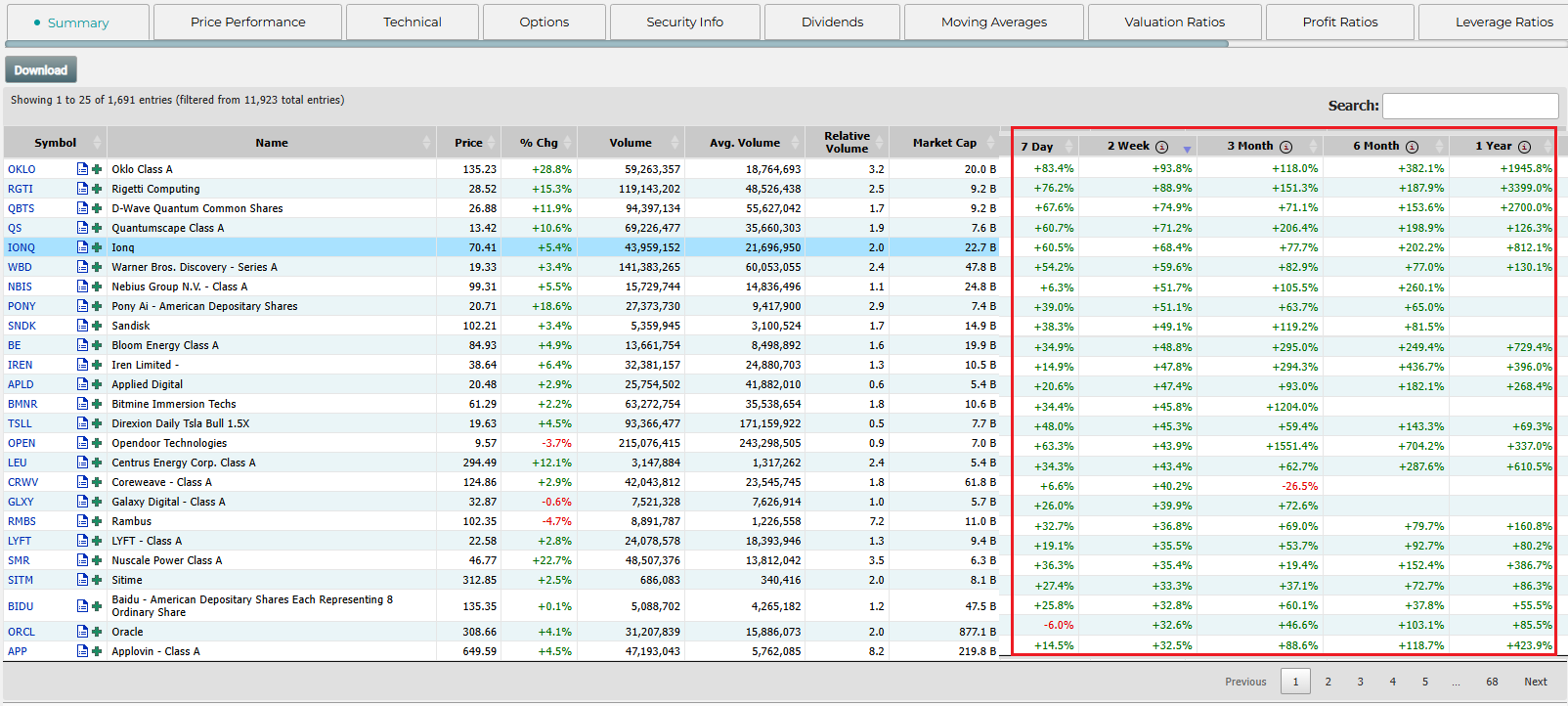

And quantum computing, another far off dream but adored by retail, these stocks have left the atmosphere and are orbiting Endor, check out a screen of the best recent perf of stocks over $5B in market cap, quantum stonks leading the pack, the 2-week returns ludicrous:

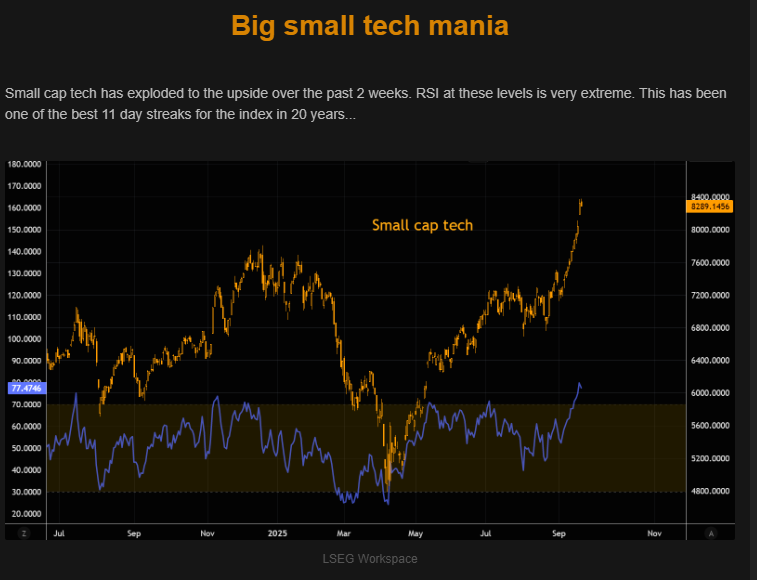

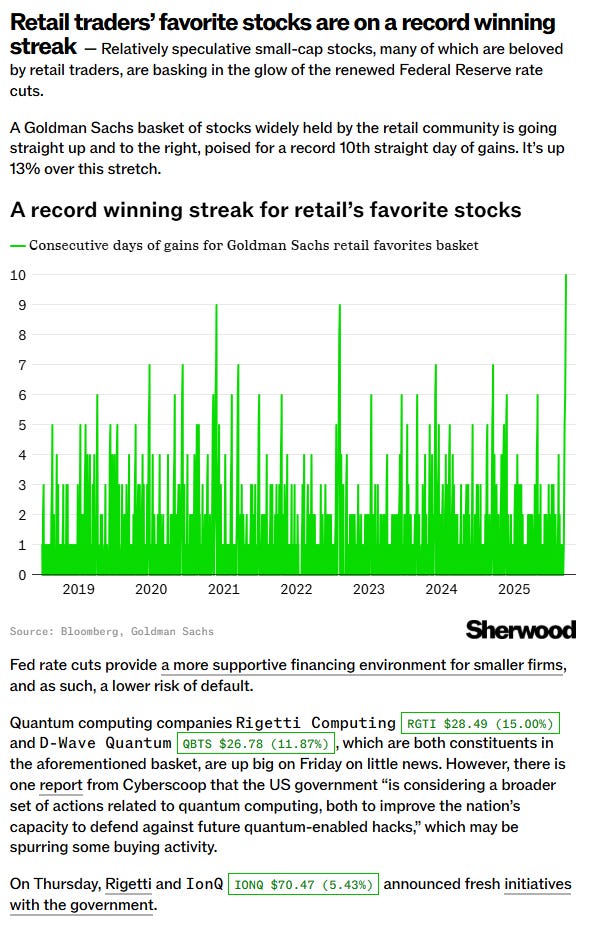

In general, small cap tech stocks have as a group gone parabolic:

Best 11 (12 now actually after Friday) day win streak in 20 years, you read that right. This is corroborated by a record streak of winning days for a general basket of beloved retail stonks:

I could go on, but that is more than enough evidence of retail exuberance, wouldn’t you say? Let’s move on to the larger investors, otherwise known as the dumb money, since they have been repetitively trounced in performance by retail. All that CFA/CPA dogma inflicting them with the diseases of prudence and pragmatism. (See the quote at the top again.)

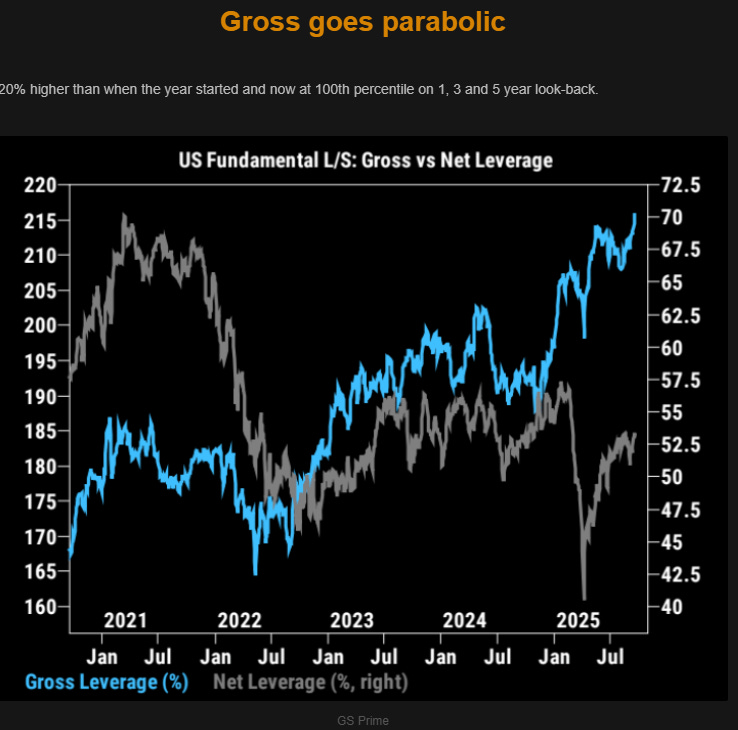

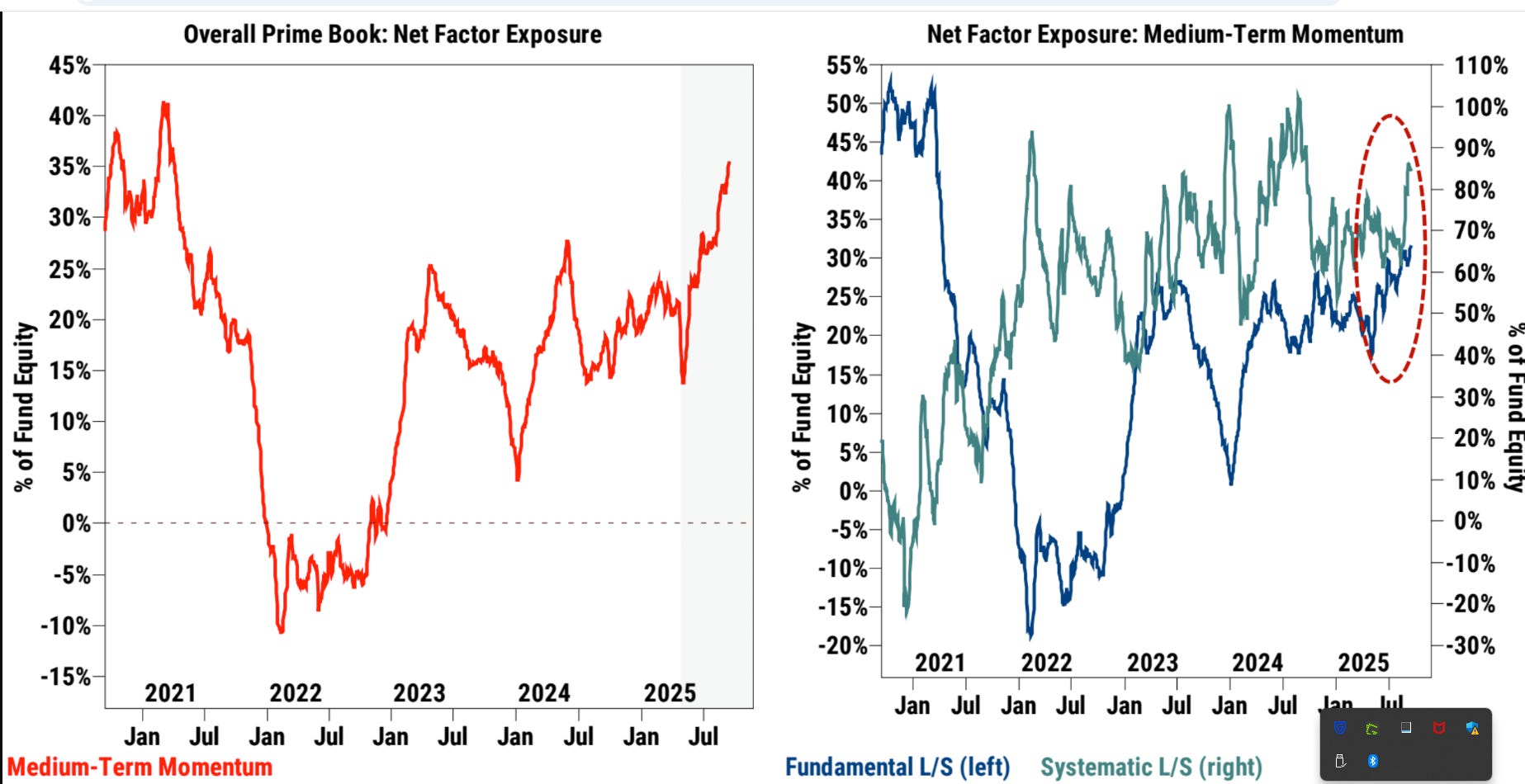

Well hedge fund gross leverage is in the 100th percentile now:

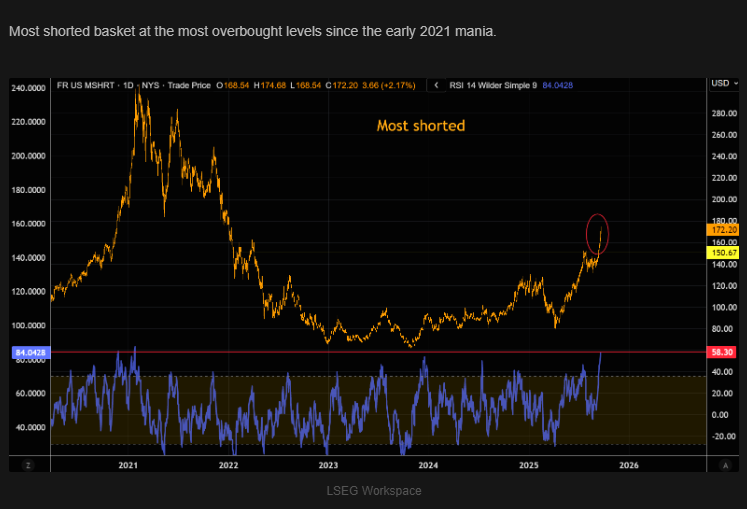

At the same time, they got squeezed in a major way this past week, forced capitulation on shorts:

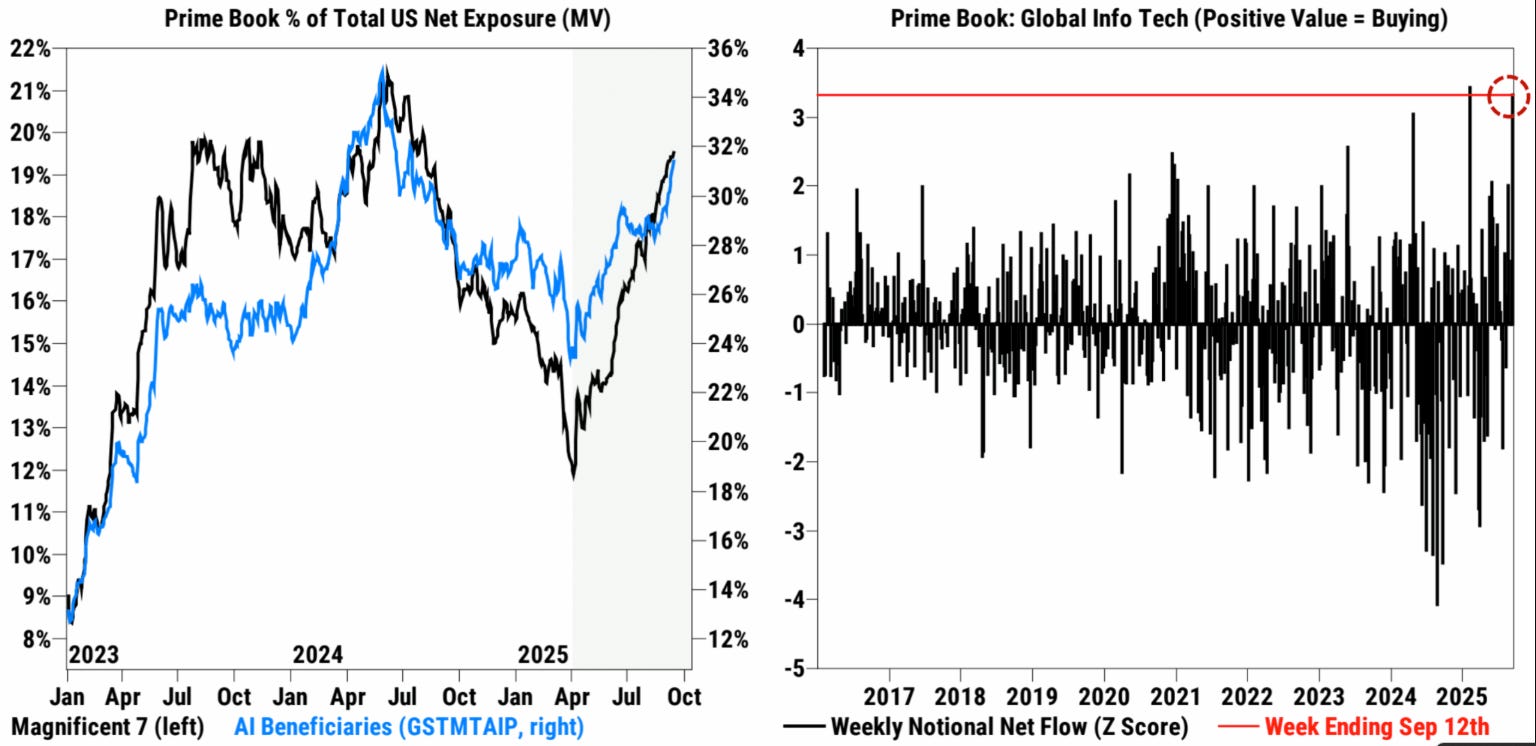

While they have continue to herd into giga tech stocks after a recent buying splurge into AI/momentum:

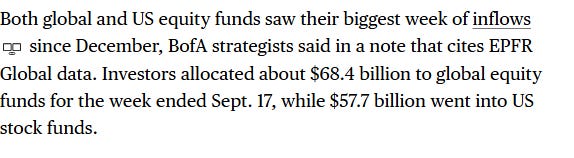

And it continued this week as $57B went into U.S. stocks:

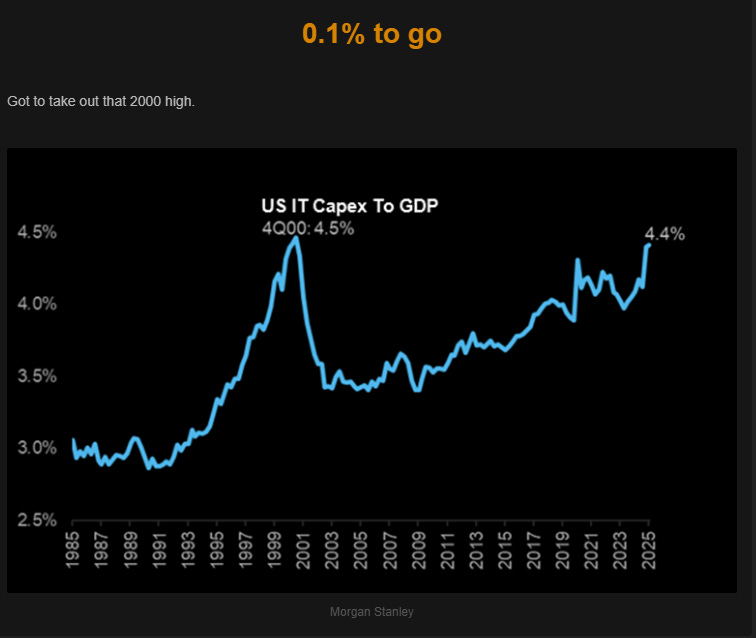

As an interesting aside, capex levels in those stocks are hitting record levels comparable only to….well you know:

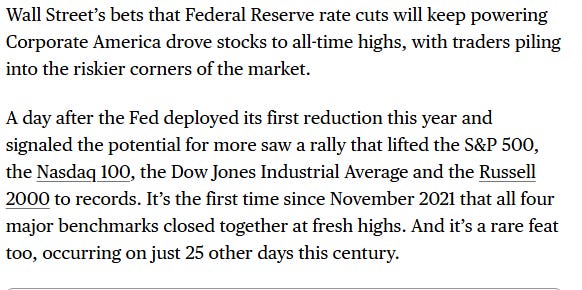

To put a couple cherries on this extreme positioning sundae, only 25x this century have the SPX/NDX/RUT2k all finished at records on the same day:

https://www.bloomberg.com/news/articles/2025-09-17/stock-market-today-dow-s-p-live-updates

Yes, 2021. That risk on fall into winter keeps coming up as a comparison. And, volumes in markets Friday were the third highest EVER:

https://www.bloomberg.com/news/articles/2025-09-18/stock-market-today-dow-s-p-live-updates

I suspect a lot of deep in the money calls in stocks were exercised Friday - folks bought calls to gain right tail exposure and now they have them at lower price points, mission accomplished. But that means larger gross exposure and the need to hedge that, as well as stocks needing to prove their worthiness into earnings season at much higher prices than the last earnings season in July. This could put pressure on the market next month; put structures being bought mean dealer selling the underlying to dynamically hedge.

All the while vol is atypically low for this time of year: